Are eMSPs the rising stars in accelerating the energy transition?

Written by Florian Thon

The Hague, The Netherlands - Transportation is still heavily dependent on energy from fossil fuels; electrifying and supplying the transportation sector with green energy is an opportunity to reduce its 7.29 gigaton-strong carbon footprint, which represents 17% of global greenhouse gas emissions and a quarter of total energy consumption in developed economies. Not much news here.

Far more interesting is the next phase in the energy transition in which the growing bank of electric vehicle (EV) batteries are used as buffers and storage for balancing the electricity grid, as we find ways to accommodate the intermittent nature of renewable energy. The final iteration is most intriguing of all: the opportunity to trade grid balancing potential between the EV charging ecosystem and the broader electricity grid. With our focus on scalable software that does good for either people or planet, we find the sector very interesting!

Storage Starships

Within transportation, passenger vehicles account for 45% of emissions. A share that is significantly higher than that of aviation or shipping – both at around 10% each. Demand for passenger transportation is increasingly being met by the accelerated roll-out of EVs. By 2030, EV batteries could provide storage capacity for up to 40% (!) of the EU’s daily average energy demand. Parties that leverage this storage capacity can make an important contribution to the energy transition, while at the same time capturing a share of a billion-dollar market opportunity.

Coordinating the flow of energy in the EV charging value chain in a way that maximizes storage of green energy during times of oversupply and use of green energy during peak demand periods is a crucial opportunity to further drive the electrification of transportation, and the energy transition.

Taking into account insights from industry insiders, we have assessed the EV charging value chain and identified the parts most likely to play a key role in this transition. In particular, electric Mobility Service Providers (eMSP) emerge as prime candidates to leverage this opportunity and as another example of scalable software solutions being used to do good.

So, are eMSPs the rising stars in accelerating the energy transition?

Complex Constellations

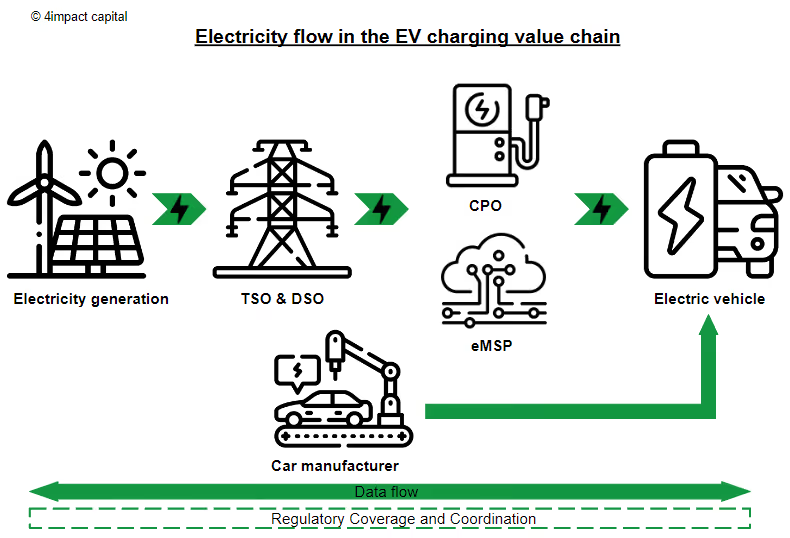

To clarify the role of eMSPs, it is helpful to first identify the other parties involved in the EV charging value chain. This value chain is somewhat complex, as there are multiple independent parties involved and technical standards between parties need to be met to a precise degree. The following parties make up this system:

- Electricity generators like enel, who generate electricity from renewable or non-renewable energy sources;

- Grid operators (transmission system operators and distribution system operators; TSO and DSO, respectively), who transmit electricity from point of generation to point of consumption; e.g. TenneT, the only TSO in the Netherlands or RWE, a German DSO;

- Charge Point Operators (CPO), who (own,) run and maintain EV charging stations, e.g. IONITY;

- Electric Mobility Service Provider (eMSP) providing the EV charging services to drivers, e.g. Plugsurfing;

- Electric vehicle manufacturers (OEMs) like Volkswagen, Audi, Hyundai, or Vinfast;

- Legal authorities, who create the legal framework surrounding the EV charging value chain, such as the European Union and European Commission.

The mentioned participants manage the flow of electricity. In parallel, another key flow is occurring, without which the EV charging process could not function: the flow of data. During the charging process, an immense amount of data is generated at the downstream end of the value chain (i.e. when, where, how much). This data needs to be communicated between the different value chain parties and can inform subsequent actions that optimize the flow of electricity.

Timing the Big Bang

As depicted in the graphic above, eMSPs form the link between data origination (the EV/the EV driver) and data use (the rest of the value chain) and therefore enable both the flow of data and electricity.

While most eMSPs currently focus on simple charging services (charging applications, payment and billing services), we expect they will venture into smart charging and/or bidirectional charging in the near future. Smart charging adjusts charging to times with high electricity supply (peak shaving), like postponing the EV charging process to midnight instead of 5 o’clock in the afternoon, when electricity demand peaks from people returning from work, plugging in their EVs, and turning on their TVs. Furthermore, bidirectional charging (also known as Vehicle-to-Grid) turns EVs into an active part of the electricity grid through coordinated charging and discharging activities.

To take full advantage of the grid balancing potential held by EVs, this energy must ultimately be exchanged with the broader market. It is unlikely that individual EV drivers will do this trading themselves. Instead, a flexibility aggregator will probably collect capacity across EV drivers and manage charging and discharging at scale, providing indispensable grid balancing. Both smart and bidirectional charging are therefore considered key technologies in the future of EV charging.

With a direct interface to the rolling fleet of EV batteries, EV drivers, and their data, eMSPs are well positioned to become flexibility aggregators and trade their network’s capacities with the rest of the electricity grid, effectively becoming energy traders.

Dimensional Disarray: Obstacles to Scaling

Despite the immense opportunity, there are several technological and legal obstacles to overcome before both charging technologies can be deployed at scale.

While smart charging is technologically possible today, bidirectional charging needs further adjustments of value chain participants like CPOs and OEMs. The latest communication protocols (i.e. the way in which standards governing EV charging are implemented across different parties) need to be adopted by all key parties to ensure data is transmitted without loss of information. Yet, difficulties frequently arise from parties not following protocols correctly, either due to lack of knowledge or improvisation of the implementation.

As the connecting element in the value chain, eMSPs have an opportunity to move parties in the value chain towards proper implementation of communication protocols and can introduce efficiency into the data flows in the value chain.

On the legal side, the market still requires a comprehensive framework defining rights and responsibilities of different parties and administrative processes like multi-currency payments or taxation. According to industry insiders consulted by 4impact, it could take around five to seven years until all legal requirements are set on the EU level and bidirectional charging can be implemented at larger scale.

Rising Stars out of a Red Ocean

The coordination challenges on the technology and legal front are poised to dominate the market for the years to come. eMSPs can capitalize on this impasse if and when they obtain an advantageous market position, which define with three characteristics: scope of network coverage (number of charge points and EVs covered), quality of customer services (e.g. billing and payment), and strategic independence (e.g. DCS Digital Charging Solutions may be limited to BMW- and Daimler-affiliated networks).

However, obtaining a relevant market position is not easy in what is becoming a red ocean market: new startups continue to emerge and raise venture capital funding at a high pace, suggesting that entry barriers for eMSPs are relatively low. We observe incumbents losing customers to new entrants who edge them out on quality of customer services, for instance. This is a market in flux, and the competitive landscape may look very different five, ten or twenty years into the future.

Flux and Expansion

Constant change in the market also means blurry lines between the different companies. Approaches differ between go-to-market strategies, operational focus (hardware vs. software), or specialization in certain business activities (e.g. payment processing). Some companies have also started integrating along the value chain into selling and/or operating charge point infrastructure. Ambitions in smart and bidirectional charging have also been announced by several players in this space.

A market segmentation might look as follows:

B2B(2C) go-to-market strategy, i.e. selling to utilities, CPOs, OEMs, or fleet operators:

- Jedlix: eMSP out of Rotterdam offering comprehensive charging services with expertise in smart charging and virtual power plants

- Deftpower: up-and-coming startup from Arnhem covering a wide range of services, with competences in smart charging

- Digital Charging Solutions: full-service white-label software solution with the largest roaming network in Europe; coming out of a BMW and Daimler joint venture, based in Munich

B2C go-to-market strategy:

- elvah: EV driver-focused charging app and services, giving access to a broad network of charge points

- ev.energy: end-to-end software platform with a wide range of charging services and ambitions in smart and bidirectional charging, B2C and B2B products

- carge: EV charging app simplifying access to and payment processes at charging points throughout Europe

Offerings beyond eMSP:

- PowerD: Amsterdam-based startup covering charge point hardware, software, and installation services

- Virta: all-in-one solutions provider out of Helsinki for EV charging businesses, including hardware and software

- JUCR - easy-install EV chargers with over-the-air software updates and bi-directional charging capabilities; based in Berlin

The value that investors and corporates attach to eMSP startups is evidenced by the recent market activity. Monta, a Charge Point management SaaS founded in 2020, raised $50m at a valuation of $155m, Virta raised €30m in 2021, and Plugsurfing and driivz were acquired for $75m and $200m respectively, indicative of the wealth of opportunities in this space.

Stellar opportunities for eMSPs

As outlined above, a great opportunity presents itself to those who can manage and trade the flows of electricity within the EV charging ecosystem to the broader electricity grid. While the regulatory framework is still not fully formed and eMSPs currently only derive a small part of revenues from energy trading, the future opportunities for flexibility aggregators seem promising. eMSPs have leverage over the technical (implementation of communication protocols) and legal (regulatory consolidation; though to a lesser extent) obstacles in the market and can use this position to hoist themselves into market leadership.

Aside from eMSPs, other parties will not be blind to these opportunities. Lateral movement or consolidation along the value chain is likely. Promising enormous impact and commercial potential, the opportunities are there to be taken, and there to be missed.

If and when the right competitive strengths are built and cultivated, eMSPs may just be the rising stars to accelerate the energy transition as flexibility aggregators. We look forward to supporting the passionate founders and teams building the future leading companies in this space!